On August 14, 1935, President Franklin Delano Roosevelt signed the Social Security Act into law. BPAS would like to recognize the 90th anniversary of this event.

Brief Historical Facts

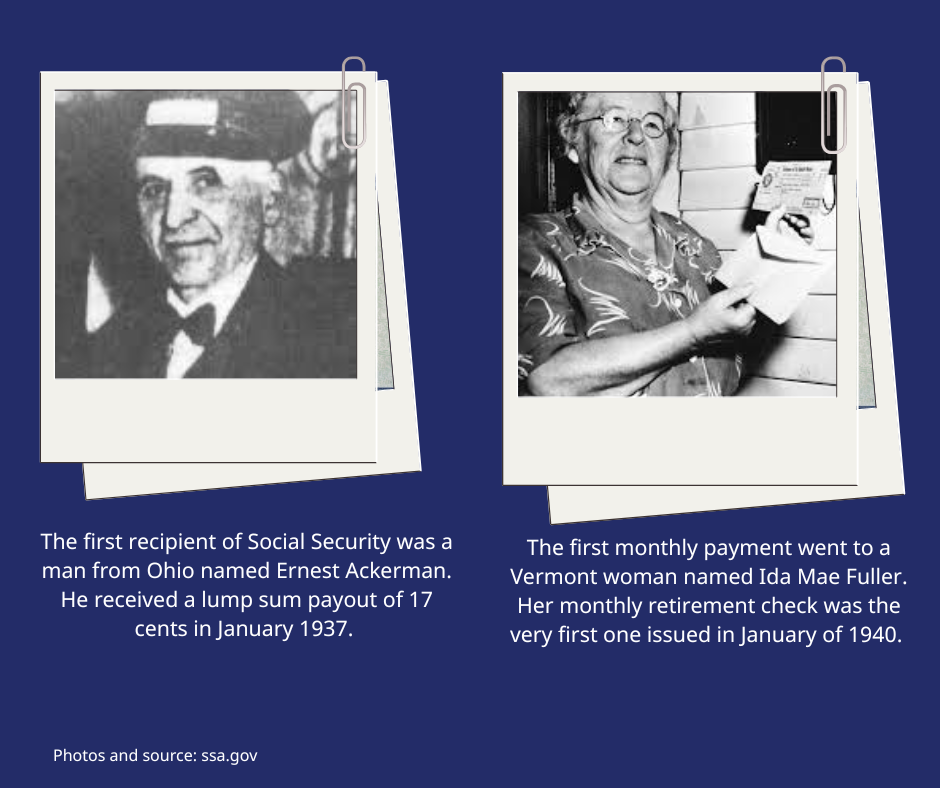

Taxes under the Act were first collected in January of 1937. In 1937, the original contribution level was 1% of earnings, made by the employee and 1% made by the employer, up to an annual maximum level of earnings of $3,000. As time has progressed, the percentages contributed by the employer and employee have increased, as well as the annual maximum level of earnings. Annual Cost of Living adjustments were added in 1975; prior to that time, benefits were increased periodically by acts of Congress.

Under the 1935 law, only retirement benefits to the primary worker were included. A reform in 1939 added survivor’s benefits and benefits for the retiree’s spouse and children. Disability benefits were added to the program in 1956.

During 2024, approximately 184 million workers had earnings covered by Social Security and were paying payroll taxes to Social Security. Currently, the taxes are 6.2% for covered employees and 6.2% for employers, up to a maximum level of earnings each year.

At the end of 2024, there were approximately 68 million beneficiaries receiving Social Security benefits.

1983 Reform

As 1983 was approaching, projections indicated that the Social Security Trust Fund would be depleted by 1983. A Commission was formed, chaired by Alan Greenspan, to investigate the long-term solvency of Social Security. The Commission recommendations were the basis of the 1983 Amendments. Highlights of the changes made at that time included:

- Accelerating a previously enacted increase in the payroll tax,

- Additional workers were added to the system,

- The full retirement age was slowly increased from age 65 to age 67,

- Up to ½ of the value of the Social Security benefit, above certain thresholds, became subject to income tax, with those tax dollars being returned to the Social Security program. (This provision was further adjusted in 1993 under the Omnibus Budget Reconciliation Act.)

Note that some of the additional workers added to the system included members of Congress, the President, Vice President and federal judges.

In 1984, the percentages contributed by the employer and employee were increased to 6.2% apiece. In that year, the annual maximum level of earnings was $37,800. The percentages of income have stayed the same in total since that time, although the amount being allocated separately to the two parts of Social Security: the Old-Age and Survivors Insurance (OASI) program and the Disability Insurance (DI) program, have been modified over the years. The annual maximum level of earnings is now automatically adjusted each year. In 2025, the annual maximum level of earnings that is taxed is $176,100.

2025 Information

Today, based on the 2025 Trustees Report, the Social Security actuaries project that on a combined basis (meaning combining OASI and DI together), the Trust Fund Reserve will be depleted in 2034. At the time of the projected depletion, the income to the system will still support an estimated 81% of benefits.

What is important to note is that the Social Security actuaries have been projecting a Trust Fund Reserve Depletion date between 2033 and 2035 for the last 14 years. And a depletion date between 2029 and 2042 over the last 35 years. So the fact that the Trust Fund Reserve will be depleted without Congressional action has been a known fact for many years.

Congress will need to take legislative action for any changes to the program to be made.

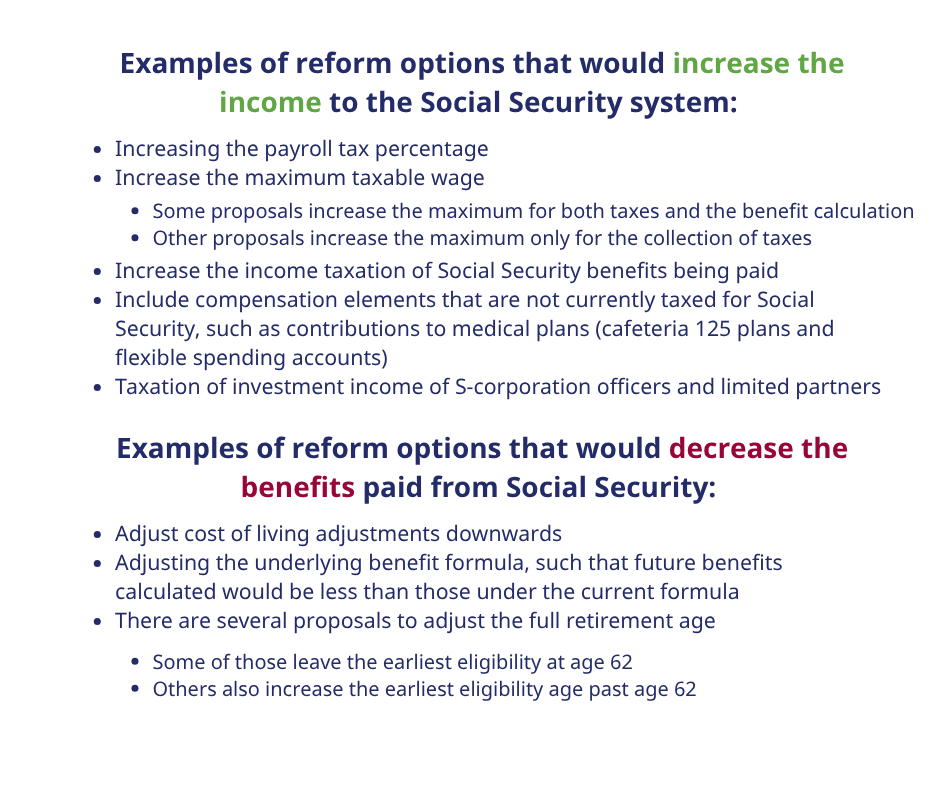

There are two ways to bring Social Security into financial balance. Either taxes will need to be increased, or benefits will need to be decreased. A combination of these could also provide financial balance.

Based on the 2025 Trustees Report, if an immediate increase in the payroll tax was implemented from 6.2% to 8.025%, for both the employee and employer, the system would be in financial balance. Alternatively, if all benefits of the system were reduced immediately by 22.4% the system would be in balance.

If changes are delayed, the increase in the amount of additional tax needed increases, or additional benefits will need to reduced. Therefore, the sooner Congress acts will provide less dramatic changes and more time to implement those changes.

Reform Options

BPAS would not be able to recommend any reform measure over another, but here are some reform options that are being discussed.

Note that the Social Security website values many different proposals, and updates the calculated values annually after the Trustees Report is published. Further, as bills are proposed in Congress, the Office of the Chief Actuary of Social Security values the impact of those on the financial status of the program and publishes those on the website.

What Should be Done to Bring Social Security Into Financial Balance?

It is important for constituents to contact your senator and congressional representative to express the need for changes to the system and for urgency in making changes in order to bring the system into financial balance.

Sources: 2025 Social Security Trustees Report and https://www.ssa.gov/history/