Find answers to common retirement account questions.

You can find your account balance by logging into your account at u.bpas.com. Your current balance will display on the home page after you enter your username and password. If you aren’t able to locate your online account login, call the Participant Service Center at 1-866-401-5272.

You can always find the status of any such request by logging into your Participant Account and navigating to the My Account menu, and under Loans or Withdrawals, select the History menu.

Because your plan is regulated by the IRS, maximum contributions change from year-to-year (indexed for cost of living increases). To see the latest figures, select IRS Cost of Living Adjustment Figures from the Planning menu. You can also find this information here. This chart will show you the amount you can contribute each year, including the additional “catch up” contribution that can be made by employees who will be age 50 or older in the current plan year. You can also access the IRS webpage (irs.gov) for additional information.

If you’re an Active employee (still employed with the Employer sponsoring the Plan), please update your address with your Human Resources division. The new address is provided to us each payroll period to update our records.

If you are a participant who has terminated employment, there are several ways you can update your address at BPAS:

1. Login to your Participant account. Under My Profile, select Personal, and then you can edit your address information online (the recommended approach).

2. Mail acceptable proof of your address change to us at: BPAS | 6 Rhoads Drive, # 7| Utica, NY 13502. Or fax to 315-292-6450. Acceptable proof of address change includes any of the following:

> Driver’s license, learner’s permit, or DMV-issued photo ID card showing your new address

> Payroll stub issued by an employer within the last two months showing your new address

> Utility bill (e.g., gas, electric, sewer, water, cable or phone), not more than two months old, issued in your name and showing your new address. Please note that we can’t accept cellular phone or pager bills

> Voter registration card showing your new address

> Current homeowner’s insurance policy or bill showing your new address

3. Complete a change of address form at USPS.com; or manually send us a change of address form from the U.S. Postal Service.

If you faxed or mailed loan or withdrawal paperwork, you may check the status of your request online by logging into your Participant Account. Or, call the Participant Services Center at 1-866-401-5272.

You may be eligible for a loan or withdrawal from your retirement account depending on the provisions of your retirement plan. Login to your Participant Account, or call the Participant Services Center at 1-866-401-5272 to see if you’re eligible.

If your employer allows online contribution changes, login to your Participant Account. In the My Account section, select Change under the Contributions menu. You may also make changes using our Automated Phone System by calling 1-800-530-1272. When prompted, simply enter your SSN and PIN, and then listen for the appropriate prompts for contributions.

If your employer doesn’t allow online changes, login to your Participant Account and print a Contribution Rate Change form from the Library. You’ll need to return your completed form to your Human Resources Department.

Follow the instructions on the login screen to reset your password.

If you qualify for a withdrawal, most plans allow you to login to your Participant Account and choose Request from the Withdrawals menu under My Account. You may access and print the forms. If you don’t have access to a printer, you can request that the paperwork be mailed.

First, take a look at your plan provisions to make sure your plan allows loans and verify the type of loan allowed. If your plan allows traditional loans, login to your Participant Account and select My Account and then click Loans. Enter the loan amount and repayment terms to determine the loan payment. After you submit the loan amount and repayment terms, you’ll be able to print the loan application to complete and return for processing. Send your completed forms to us at the address or fax number shown on the cover page of your application form or upload via your online account.

For MyPlan Loans, if spousal consent is required by your plan, you’ll also need to complete and send a Spousal Consent Form.

You may pay off your payroll-deducted loan by sending us a cashier’s check, money order, or personal check along with a Loan Payoff form. You may find a Loan Payoff form under the Library when you login to your Participant Account. Payments made by cashier’s check or money order are processed within 1-3 business days of our receipt. We’re required to hold personal checks for 10 business days. Please make checks payable to the name of your retirement plan and mail to:

BPAS | 6 Rhoads Drive, #7 | Utica, NY 13502

You may pay off your MyPlan Loan by logging into your MyPlanLoan account to make an electronic payment. Or, you may send us a cashier’s check, money order, or personal check and indicate in the memo section “MyPlan Loan payoff.” Please note there is an additional fee for payments that are mailed. You can mail payment to:

BPAS | 6 Rhoads Drive, #7 | Utica, NY 13502

If you are looking to pay off a defaulted loan, please contact Participant Services at 1-866-401-5272, option 3, so they may provide you with a 10 day payoff amount.

We suggest you contact your plan’s financial advisor for investment guidance. If you don’t know your advisor, please call us at 1-866-401-5272 so we can provide you with the contact information.

For security purposes and your protection, we’re not able to email documents containing personal and financially identifiable information. We’re currently investigating options that may allow us to email this information securely in the near future.

Vesting is the percentage of a retirement account that is “owned” by a plan participant; you’re only entitled to the amount you have “ownership” in.

Any money you contribute (e.g. a salary deferral or rollover contribution) is always 100% vested. Employer contributions, however, may be subject to a vesting schedule. The rate at which Employer contributions vest is dependent upon your Plan’s provisions. More information about your Plan’s specific vesting schedule can be found in the Summary Plan Description in the Resource Center.

If your account shows two different balances (your Total Account Balance differs from your Vested Account Balance), it’s because your Employer contributions are not fully vested (owned by you) yet.

Your Employer enlisted BPAS AutoRollovers to establish IRAs on behalf of terminated participants. Because you no longer work for the Plan’s sponsor (the Employer), and your account balance is below a certain threshold, we rolled your funds to a new account that’s safe and fully accessible to you. The difference is that your new account is no longer associated with your former Employer’s plan. Please call the Participant Services Center at 1-866-401-5272 if you have questions regarding your new IRA account.

We are required by the IRS to mail 1099-R forms no later than January 31. If for some reason you haven’t received your 1099-R by February 15, please call the Participant Services Center right away at 1-866-401-5272 or login to your Participant Account and download your form. The forms will be found in the Library under Tax Forms.

Yes. We have a number of team members who are fluent in Spanish, and stand ready to assist if needed. Furthermore, we utilize translation services that can be conferenced in if necessary.

Our website can also be viewed in Spanish, and we have a number of Notices and other materials that can be provided in Spanish as well.

If you don’t wish to participate in the retirement plan at this time, you may change your deferral amount online, if your plan allows, or by calling the Participant Services Center at 1-866- 401-5272. If your plan doesn’t allow online changes to your deferral election, you may login to your Participant Account and print the Contribution Rate Change form from the Library. Return the completed form to your Human Resources Department.

Roth Elective Deferrals and After Tax Contributions are similar in tax treatment initially and during the years before retirement. The main difference involves tax treatment of withdrawals.

We require the Rollover Verification Form for all rollover assets; the trustee of your former employer’s plan also requires paperwork to initiate a distribution. If you completed both forms, it’s possible we simply haven’t yet received the assets from your previous plan administrator. We suggest you contact the trustee of your former plan to ensure they have the necessary paperwork and have forwarded your assets to BPAS.

Just contact our Incoming Rollover Specialist at [email protected] or call (866) 401- 5272, ext. 35007. You may even fill out the BPAS Rollover Verification Form electronically to speed-up the process. Our Rollover Specialist can also help you contact the trustee of your former employer’s plan by hosting a 3-way call.

You may request a withdrawal from certain money sources prior to termination if you are facing a heavy and immediate financial hardship. Please review the Hardship Distribution Form for information regarding any applicable documentation, tax withholding rules, and/or penalties that may apply to you. Below are details of what documentation may be submitted or what you should retain in case of audit.

Documentation for Purchase of a Principal Residence

> A copy of the binding contractual agreement (including addendums, if any) to build a home or a purchase agreement that is signed and dated by both parties (buyer and seller). These agreements must include the address of the property, the total purchase price, and a future closing/settlement date not to exceed 90 days from the request date.

> Purchase of Land (for purposes of building a primary residence): A current bill of sale, contract or deed indicating a future closing/settlement date, must be signed by buyer and seller, dated and include address of property.

> Building Primary Residence: Copies of the costs directly related to building a primary residence, such as invoices or bills including any material costs that need to be paid.

> One of the below documents to verify the “Estimated Costs Due at Closing.” The purchase price and the property address listed on the below document MUST match the purchase price and property address listed on the purchase agreement:

> > The “Initial Fee Worksheet” (dated within 45 days) containing the participant’s name, the property address and the estimated costs due (out of pocket expenses) at time of closing.

> > A letter from the lender (dated within 45 days) verifying the amount of the “Estimated Costs Due at Closing.” The letter must be on the financial institution’s letterhead referencing the participant’s name, property address and it will need to be signed and titled by a representative from the facility.

> > A copy of the Uniform Residential Loan Application (dated within 45 days) containing the “Estimated Costs Due at Closing.” The loan application must contain the participant’s name and the property address. If a future closing date is not on the sales agreement, the participant must provide a letter from the mortgage company that includes the future closing date. The letter must be on letterhead and reference the participant’s name, the property address and it must be signed/titled by a representative from the mortgage company.

Payment of Tuition & Related Fees

Definition: Payment of tuition, related educational fees, and room/board expenses, for up to the next 12 months of post-secondary education for the employee, employee’s spouse, children or dependents.

Post-secondary education generally refers to education that commences after the completion of high school. Expenses that would qualify for a hardship withdrawal would include tuition, fees charged for the use of technological or other facilities required for the post-secondary program (such as computer fees or gym facility fees), dormitory expenses and expenses of a room or apartment close to the educational facility, and meals while attending the educational program. Loan repayments of student loans are not educational expenses for this purpose.

Documentation for Payment of Tuition & Related Fees

> Copies of actual invoices for future tuition on school’s letterhead, of up to the next 12 months of post-secondary education. The bill must include: the name of the student, the name of the school or educational institution, the period for which the expenses are incurred (ex. spring 2025) and the total amount due. Unpaid invoices must be dated within 45 days and contain semester start date of no more than 90 days before the start of semester or during the semester for which expenses are incurred. Expenses for prior periods/semesters are not eligible for a hardship withdrawal.

*The tuition bill must indicate the current and/or future semesters are due along with the amount required to satisfy the need. The bill cannot be for “estimated” costs. It must be clearly indicated that the required payment is a “finalized” statement from the school.

**If the tuition bill indicates a name other than the participant’s, you may need proof of dependent or spouse. This could include tax documentation or birth certificate as proof of dependent or marriage license as proof of spouse.

> Copy of the bill for dormitory fees or housing fees (or estimate of dormitory fees that is signed by the educational institution) that appears on the school’s letterhead containing the name of the dormitory or housing provider and the name of the participant or student. A copy of a lease agreement indicating the rent and signed/dated by all interested parties. The bill must specify the amount due and must refer to a future period ending not more than one year later than the date of submission.

> Copy of the bill for board or meal expenses (or estimate of boarding expenses that is signed by the owner or manager of the boarding establishment) that appears on the school’s letterhead containing the name of the establishment providing the board and meals and the name of the participant or student. The bill must specify the amount due and must refer to a future period ending not more than one year later than the date of submission.

Payments to Prevent Eviction or Foreclosure

Definition: Expenses necessary to prevent the eviction or foreclosure of the employee’s primary residence. The participant can only qualify for a hardship withdrawal for this reason if a specific dollar amount is due by a certain date in the future in order to prevent foreclosure or to avoid eviction.

Documentation for Payments to Prevent Eviction or Foreclosure

> A copy of the eviction/foreclosure notice or court order. The notice or Court order must:

> > Include the participant’s name and address (address on documentation must match address on record).

> > Be dated within 45 days of the request.

> > Clearly state a future date by which the amount is due to prevent Eviction or Foreclosure.

> > Provide the months for which the rent or payment is due.

> > Clearly identify the Landlord’s name and the Landlord’s contact information.

> > Include the Landlord’s dated signature and TITLE (e.g.,Landlord, Property Manager, etc.).

> > The Landlord’s signature needs to be witnessed by a Notary Public if the eviction letter is not on Letterhead of the complex/company.

*The letter should indicate a future date of when the funds for mortgage or eviction are due, it is okay to accept it as long as the date on the letter is current and not older than 14 days. The letter must indicate that foreclosure/acceleration proceedings may or will take place if the funds are not paid.

> If the address on record does not match the address of the primary residence on the foreclosure or eviction notice, the participant needs to have a copy of their current driver’s license showing the primary residence address. If the current driver’s license has not yet been updated with the primary residence, the participant may also submit a signed, dated, notarized letter stating that the home in foreclosure, or the residence that the participant is being evicted from, is the primary residence.

> If the name on the foreclosure or eviction letter does not match the participant’s name, supporting documentation should be retained indicating that the participant lives there. This will include a copy of an income tax return or a utility bill.

> A copy of the foreclosure notice from the financial institution (on the financial institution’s letterhead) or Court Order (dated within 45 days). The notice or Court Order must clearly state the dollar amount that is due and a future date that it is due in order to remedy the foreclosure proceedings.

> Delinquent property taxes qualify if they are taxes on the participant’s primary residence and will result in foreclosure or sale of the property. The tax notice (dated within 45 days) must reference the tax year(s); it must state the dollar amount due and a future date that is needed to prevent the sale of the property.

Medical/Dental/Hospital Expenses

Definition: Expenses for (or necessary to obtain) medical/dental/hospital care that would be deductible under IRC section 213(d) (determined without regard to whether the expenses exceed 7.5% of adjusted gross income). The participant may request a hardship withdrawal for qualifying medical expenses incurred by the participant, the participant’s spouse, children or dependents.

Medical/Dental/Hospital Care includes unpaid amounts for any of the following:

> For the diagnosis, cure, mitigation, treatment or prevention of disease, or for the purpose of affecting any structure or function of the body.

> For transportation primarily for and essential to medical care.

> For qualified long-term care services, which include necessary diagnostic, preventative, therapeutic, curing, treating, mitigating, and rehabilitative services, and maintenance or personal care services. To qualify, these services must be required by a chronically ill individual and provided under a plan prescribed by a licensed health care practitioner.

> For insurance covering medical care as described above, or for eligible long-term care premiums for any qualified long-term insurance contract.

> For lodging away from home that is primarily for and essential to medical care, subject to the limits of IRC section 213(d) (2).

> For prescribed drugs that require a prescription of a physician.

Documentation for Medical Expenses

> Medical/Dental/Hospital Expenses: Copy of the medical/dental/hospital bill listing the medical/dental/hospital expenses and totals on letterhead of the medical or insurance provider showing the participant or the dependent as the patient or insured. Bill must not be older than 90 days. Itemized insurance and medical/dental/hospital bills must show the insured and uninsured portion of the expenses. If doctor, hospital, or other health care bills are not covered, the provider must verify thie information directly on the medical bill in addition to signing and providing their title. If the bill indicates a past due date, the participant needs to have an updated bill.

*If the physician/dentist refuses to perform future treatment without payment in advance, the participant needs to include a signed treatment plan from the doctor’s office. This must include the title of the person signing, stating the future date of the appointment and that payment is expected at the time service is rendered. The treatment plan must show the estimated insurance portion and the amount due by the patient.

**If the bill is in the name of anyone other than the participant, proof of dependent is needed. This includes either the participant’s tax documentation indicating proof of dependent or the dependent’s birth certificate.

> Long-term Care Services: Copy of the service bill listing the services and dollar amounts of expenses on service-provider letterhead or insurance provider showing the participant or the dependent as the patient or insured. Itemized insurance and medical/dental bills must show the insured and the uninsured portion of the expenses. Bill must not be older than 90 days.

> Insurance Premiums for Medical Expenses or Long-Term Care Services: Copy of insurer’s bill for premiums on letterhead showing the participant or dependent as the patient or insured. These premiums must not be reimbursed by any Employer. Bill must not be older than 90 days.

> Lodging Expenses while away from home primarily for essential medical care: Copy of the bill from provider on letterhead showing the participant or dependent as customer with accompanying medical expense bill indicating the dates of service. Bill must be dated within 90 days and participant can only submit lodging expenses up to $50 per person, per night.

*Medical care does not include cosmetic surgery or similar procedures, unless it is necessary to ameliorate a deformity related to a congenital abnormality, a personal injury resulting from an accident or trauma, or a disfiguring disease.

Expenses for the Repair of Damage to the Employee’s Principal Residence that Qualifies for a Casualty Deduction

Definition: Expenses for the repair of damage to the employee’s principal residence that would qualify for the casualty deduction under section 165 (determined without regard to whether the loss exceeds 10% of the adjusted gross income).

A Casualty Loss is defined as a “sudden, unusual or unexpected” event resulting in an uninsured loss. Causes of such rapid losses include flood, fire, earthquake, wind damage, water damage, theft, accident, vandalism, hurricane, tornado, riot, shipwreck, snow, rain and ice.

Documentation for Casualty to Home

> Evidence of casualty (a detailed description of the events that resulted in the casualty). The participant may submit pictures and/or articles of newspaper clippings as evidence.

> The reason for the loss and any documentation supporting the loss. The participant must sign/date their letter of explanation.

> The location of the loss (the address of the loss must be the participant’s principal residence).

> If the address on file does not match the address of the participant’s principal residence in Omni as listed on the casualty description or invoices, the participant needs to submit a copy of their driver’s license indicating the primary residence address. If the current driver’s license has not yet been updated with the primary residence address, the participant may also submit a signed, dated, notarized letter stating that the home affected by the casualty is the principal residence.

> Unpaid current (dated within 45 days) invoices and/or contracts, signed by participant and contractor, evidencing the cost of the repair, and which indicates that insurance does not cover the cost of repairs. The invoice must state a future date in time when the repair will take place. The contracts must be fully executed with a representative and participant’s signatures on contract. Please note: An estimate of these charges is not acceptable proof.

> Copy of any insurance claims from your insurance company as evidence that the damages have or have not been covered by your homeowners insurance. If the participant does not have insurance and provides a cancellation notice, then we need further proof indicating that the damage was casualty loss (ex: Notice from FEMA indicating that the county the participant lives in is considered a disaster recovery). **The participant can only qualify for a hardship withdrawal for this reason when there is a casualty loss to their principal residence that arose from fire, storm, shipwreck, theft or some other casualty. Only the portion of the expense that is not covered by insurance is eligible for this purpose.

*To be deductible, a casualty loss must occur quickly, usually instantly or over a few days. Slow losses that occur over months or years, such as mold damage, dry rot, moth or termite damage, or normal home maintenance to repair or replace windows, roof or plumbing generally are not tax-deductible, and therefore do not qualify for a financial hardship.

**The participant can only qualify for a hardship withdrawal for this reason when there is a casualty loss to their principal residence that arose from fire, storm, shipwreck, theft or some other casualty. Only the portion of the expense that is not covered by insurance is eligible for this purpose.

Payment for Burial or Funeral Expenses

Definition: Payments for burial or funeral expenses for the participant’s deceased parent, spouse, children or dependents.

Documentation for Payment for Burial or Funeral Expenses

> Unpaid invoices (dates within 45 days) from other parties to pay additional expenses associated with the funeral.

> Covered expenses including opening/closing of a grave, a burial plot, a burial vault or grave liner, a marker or monument, a crypt, cemetery perpetual care charges, honoraria for clergy, a funeral breakfast/luncheon/dinner expenses associated with the funeral/memorial service, flowers, guest registers and acknowledgment cards, music and urn or casket.

> Expenses that are not covered include invoices that have been paid, burial expenses to the extent that they are covered by Veteran’s benefits, travel expenses incurred by family members to attend the funeral, and prearranged/prepaid funerals.

> Provide a copy of the current (dated within 45 days) unpaid invoice signed by the funeral home/director. The itemized bill must show the name of the deceased, the unpaid balance due and the responsible party (participant) for payment.

> Copy of death certificate.

> Proof of immediate family member (marriage license, birth certificate, etc.).

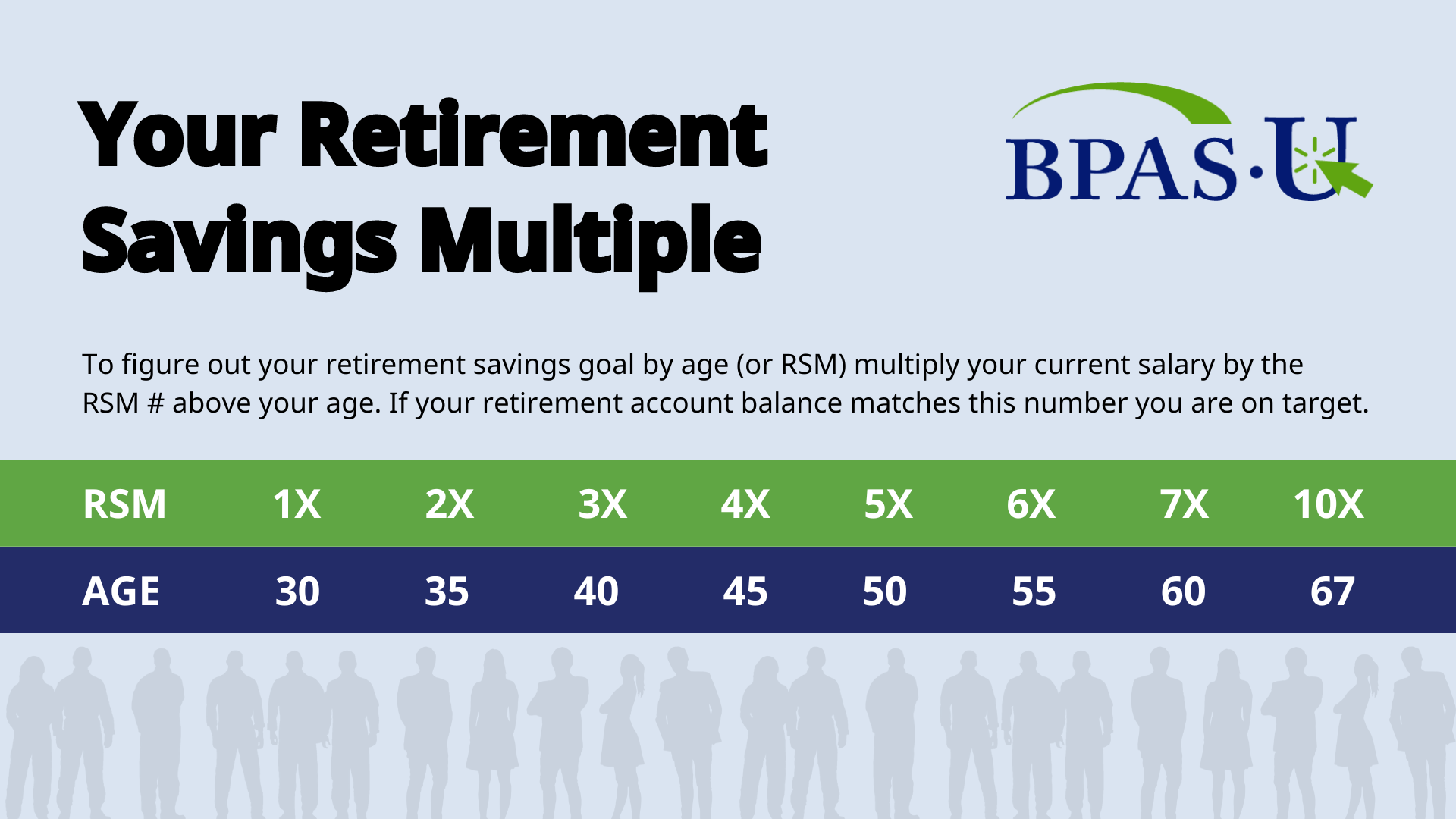

An RSM is an age-based number used to assist you on your road to retirement. It can be a quick checkpoint to see if your existing savings strategy is sufficient or should be adjusted. To try it, simply use the On-Target RSM closest to your age and multiply it by your current salary. The result is how much money you should have in your retirement accounts at this point. You can find the On Target RSM on the page 4 of your quarterly statement, which you can access at any time by logging into your account and accessing Statements located under My Account. If your account balance is more than the calculated number, your current savings strategy may help you reach your retirement goals. If your balance is below the calculated number, one of the best ways to improve your outcome is to increase your contribution rate within your retirement plan.