Thanks to enhancements under SECURE 2.0, catch-up contributions now provide even greater benefits for participants age 50 and older. The information on this page will provide you with some additional information about catch-up contributions for your Workplace Retirement Plan.

What are catch-up contributions? Why were they established? Our short video provides an explanation:

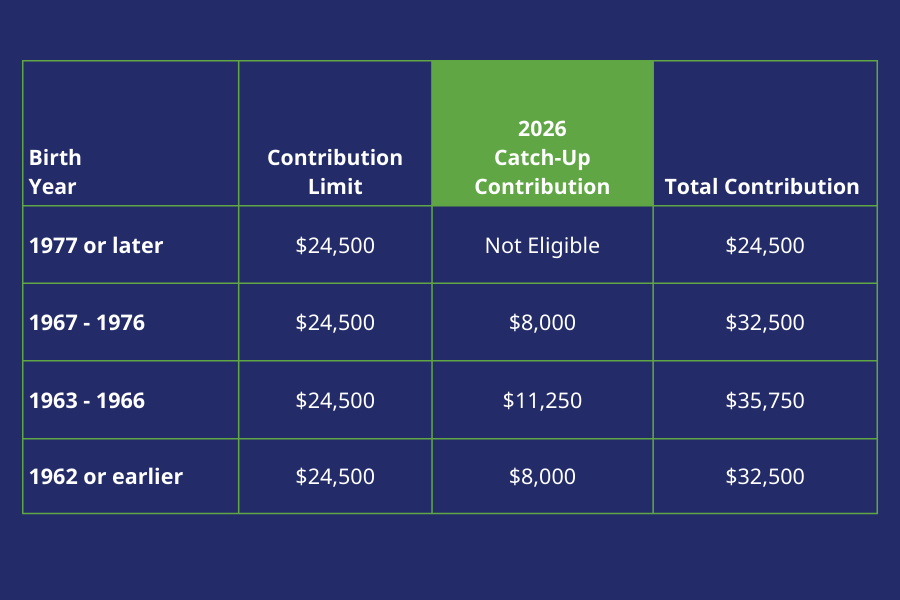

Are you eligible for catch-up contributions? And if so, how much?

Catch-up contributions are for participants age 50 or over. With SECURE 2.0 legislation, enhanced catch-up contributions were introduced for participants age 60 – 63. Review the chart below or the attached flyer to see how much you can contribute in 2026.

Roth Catch-Up Contributions

Another SECURE 2.0 legislative change: employees classified as Highly Paid Individuals (HPIs) must make catch-up contributions as Roth contributions. If your 2025 FICA wages were over $150,000, catch up contributions for 2026 must be made as Roth catch-up contributions. Review the attached flyer for additional information.